Siesta Key Vacation Rental Investments

© James Hock 2007 - 2020 NOTE: This is very long, a full book

How would you like to retire RICH?

OK, maybe not rich, let's say comfortable! (I had to say something to get your attention). But read on and see what you think.

I know, retirement is the last thing on your mind right now! In these turbulent times, who can worry about something that's 10-30 years away from now when currently it's a challenge to simply live paycheck to paycheck!

I once lived exactly like that, blowing every dime I earned keeping up with rent payments, car payments, credit card payments, and buying every new gadget I couldn't live without. Seems like we all develop a good case of instant gratification in our younger years.

By middle age (whatever that is), most of us at least start realizing that unless we want to be bagging groceries when we're 70, we better start putting a few bucks away for our older years. Some are lucky enough to have retirement plans, but unless you're a high level executive in the company, probably your retirement plan, along with Social Security, will just afford you a very modest retirement at best.

This is the true story of how I learned to focus some of my attention to my longer term financial needs, and how I stumbled on an investment that proved to be so interesting and fun, that it took the boredom out of "saving for retirement" and provided for over 20 years of exciting beach front vacations for my family and friends

As the title indicates, the fun investment I stumbled upon is owning Ocean Front Vacation Rentals on the beautiful white sandy beaches of Florida. My story will cover in detail everything you should know about Vacation Rental Investments

I want to be very clear that this is not a story about a "get rich quick" scheme (If you know how to do that, I say go for it!). Rather this is a story of how to get KIND OF WELL-OFF SLOWLY AND SECURELY. If you're still into instant gratification, perhaps this story is not for you.

Also this is not a story of how to start with nothing, and grow it into something. If you still haven't managed to save a little money, or built some assessable equity into your home, then maybe this story can only serve to motivate you with ideas you may want to consider for your future

My story is not theoretical, you will learn exactly how Vacation Rentals worked for me (and continue to work) over an almost 20 year period, through the ups and downs and turbulent financial climate we've all lived through, including the recent Real Estate Bubble and meltdown

So, just to give you a feel for where we're going with this, in 1993 I scrapped together (using some of my retirement savings, 2nd job earnings, and small loans from friends), about $65,000 to make my first "Vacation Rental" purchase.

To date, that investment has returned to me a gross of WELL OVER $1,000,000, (YES - that's ONE MILLION DOLLARS, and will continue to bring in an additional $70,000+ gross per year until I decide to sell it. Clearly a large chunk of the 1,000k gross went to pay off the mortgage debt over the years, but no matter how conservatively you look at it, with that properties value now pushing over $800,000 I will realize a great total return on my original $65,000 investment.

When I stop and think about it, I conclude that I've been fortunate to have had a good enough job to pull together 65K to invest 20 years ago. But mostly I'm struck by the incredible economic potential provided with the relatively new concept of owning "Vacation Rental Property". Many of us who spent most of our lives working for a large corporation often dreamed about owning "our own business". Some of my friends quit their secure jobs to start their own businesses, and sadly lost most of their life savings. I discovered that I could stay in my secure job and get involved in this "side business" of Vacation Rentals with a minimum of risk or work.

I'm thankful to my accountant dad, who instilled in me some degree of financial understanding, and also to our family doctor, who through a chance encounter, got me started on this interesting path.

Now back to my story. In the first Chapter I'll share a few words of financial understanding I learned from my dad, nothing complex or too boring, I promise. I'll bet you may find it fairly interesting.

In Chapter 3 we'll explain what a Vacation Rental Property is (HINT! - NOT A TIMESHARE!)

In Chapter 4 I'll relate my adventure of getting started, searching for and purchasing my first property, including sharing the actual amounts it costs and the income it generates. This will not be theory, this will be factual information.

In Chapter 5, we continue with the experiences of owning this Vacation Rental over so many years, watching it appreciate, and purchasing more.

In Chapter 6, you'll hear all about the Great Real Estate Bust and exactly how the Vacation Rentals faired here in Florida and Siesta Key.

In Chapter 7, we'll briefly examine the question of; is it too late to get involved in this Vacation Rental business?

In Chapter 8, we'll discuss the many considerations involved in purchasing a Vacation Rental Property, dig deeply into all the important details (that your Real Estate Agent won't tell you).

In Chapter 9, we'll close with lessons learned from the Real Estate Bubble and meltdown, important thoughts that will put things in a new perspective that you may have never considered.

In Chapter 10, I'll close with an update of my recent activities and my Siesta Key outlook.

If you love Siesta Key as much as we do, read on while I describe to you how you might want to consider adding Siesta Key to your Retirement Plan! (This doesn't necessarily mean that you would have to retire here, but that you might consider using our popularity to help increase your retirement assets).

Of course if you're already retired, or retirement is almost upon you, it may be too late, but If you still have 10 or more working years ahead of you before you take retirement, you may want to read on and learn how many of us owners down here have built ourselves a wonderful retirement utilizing investments in Siesta Key

To start with, let me assure you that I am not a Real Estate Salesman, and in fact have absolutely nothing I want to sell you. But I was fortunate enough many years ago to be given this advice (by my Dad and later by my Doctor of all people), and it has worked so well for me, I almost feel obligated to pass it along to others.

***********************

Chapter 1 - Dad's Advice

***********************

Dad worked as a accountant in General Motors for over 30 years. Dad often described his goal in life, which was to enjoy a retirement that lasted as long as his working years. (Dad pretty much achieved his goal).

Dad wasn't crazy about his job, so perhaps he spend more time than others complementing his future retirement and saving and planning for it. Dad taught and instilled in me an understanding of getting "someone else" to be working for me. He didn't mean opening a business and having employees, he meant accumulating some money and investing it into something that would then work for me - for the rest of my life - so I could eventually QUIT WORK and let investments support me in my later years

Dad talked about a popular book called the Secret. Although I have not read it, my understanding is that it describes a mental process that has been well known and passed down through many generations. And it really isn't much of a secret, it's more or less simply wanting something, visualizing it in your head, and magically perhaps that makes your dream come true

While certainly there is some truth to that, most of us find it's not that simple, it really involves wanting to make something happen in your life , and then actually doing something about it to make it happen. However, there is a secret to creating monetary wealth in your life that also has been known for many years, all the rich guys like Trump and Ford practice it. In recent years, a mini-version of this wealth building technique has been available to common folks who took the time to study and learn about it.

The Wealth Secret

When I used to be a smoker (40 years ago), we always used to kid about what brand we smoked, "OP's" (Other People's)!

The big secret in wealth building is simply that; use "OP" (other people's money) to buy wealth for yourself - now that's pretty simple isn't it?

Many of us learned years ago as we made our house payments, that that was a pretty safe and profitable way of using someone else's money (your mortgage ) to purchase some wealth (your home). Some of us, realizing that over the years we were accumulating more wealth in the equity in our home than we could possibility save, may have purchased additional homes, just for investments. (I don't recommend it).

Owning a Sports Team

Why is it that all the really rich people buy themselves a Football Team, or some other sports franchise, just because they're big fans? (And they always overpay for them, and endlessly cry how much money they're losing every year). So are they just careless with their cash because they're so rich, or just stupid? Probably not. They are simply practicing a safe and proven wealth-building technique that's been around for hundreds of years, and I'm about to give you the complete formula in a single sentence in the next paragraph.

The Complete Wealth Secret

Use other people's money to buy quality income-producing assets that rapidly appreciate.

That's really pretty simple, right? (The only problem is you don't happen to have enough for a down payment on the Detroit Lions, right?) (And "quality" might be questionable there - KIDDING!), So let's look in a little more detail.

There are only 4 major parts to this simple wealth formula,

Use other people's money

You already know this from your home investment; we use other people's money when we borrow funds to finance our home. The most common way to do this is with a mortgage or equity loan. But note that your home doesn't produce income, so it doesn't qualify in this time proven formula.

Quality

An interesting word, we all think we know what it means, but it is usually difficult to put into words. (If you don't believe me, read Robert Pirsig's Zen and the Art of Motorcycle Maintenance). So while quality is subjective, most of us think we recognize it when we see it. Unique - valuable - uncommon - rare - priceless

Income-producing Assets

Can be just about anything, from a Sports Team to a Shopping Mall. Many poor folks get caught here, notice that the criteria is simply "Income-producing", it is not "profit producing". The way it works in the real world is these assets will always to priced at a "reach", the fact is that you can never find a business or any other investment where the current owner will price it below it's market value (unless of course the current owner is "Dad").

Now the amount of income is important, but the real truth is whatever income-producing asset you purchase will not break-even (unless you're investing in very risky ventures that don't meet the "Quality" part and we will not be discussing here). Look at Trump, all of his Casino's and Hotels loose money, yet he keeps buying them.

Rapidly appreciate

The key is appreciation, growth of value. It is great if it is rapid, but none of us can look into the future so we have no way of measuring this other than by extrapolations of historic performance or "rules of thumb".

"Vacation Rentals" - (My Initial Learning Experience about 1990!)

Back when I lived in Michigan, where the days were gray and cold from October to April, I was constantly plagued with "sinus infections". At least 1-2 times each winter I would be sick enough to visit my family Doctor to get treated for my sinus infection. One sloppy winter day as I was in for a new prescription, I said, "Hey Doc, you live here in Michigan just like me, how come your sinuses don't make you sick like I get, I want some of that stuff you take!

"Rental Condos", he replied

"Excuse me?"

"Vacation Rentals (or Rental Condos), I have 3 of them down in Florida", he replied, "between all 3 of them, one is usually open long enough for me to fly in for a few days of Golf in the sun. I'm down there a few days twice a month or so all winter.

"Oh Yea", I replied. "Easy for you, but we all don't live on a Doctors income".

"The trips really don't cost me much at all, I book the Spirit Airline sales, often making the round trip for $150 complete, and since I own the condo unit, my room is free".

As quick as I challenged him about the fact that we all can't afford to own condos in Florida, he shot back, "You can't afford not to!" he continued, "You're probably looking forward to retiring someday, you really should look into the Vacation Rental concept".

I replied that I knew all about rental property, and hated it. (Actually in the late 1970's I owned a small 3-unit apartment and the mix of low-life tenants, broken toilets, and bounced rental checks, taught me that business wasn't for me).

Doc really didn't have time to argue, but simply said it was nothing like owning an apartment building or a single-family rental home, and that I should at least look into it. As the thought of spending time on a warm Florida Beach sounded intriguing, I told him I would

***********************

Chapter 2 - Serendipity

***********************

Funny how life works, the very next day at work in the shop, while we sat around shooting the bull, I was telling my buddies how my rich Doctor made it through our winters, and asked if they had ever heard of "Vacation Rentals".

"Actually I have", replied old Ray, "Mark, the new foreman who took over Joe's gang, was talking about them the other day, said he was about to buy one in Indian Beach Florida".

Later that day I cornered Mark and found I had an expert on the subject. Briefly I learned, Mark had purchased a Vacation Rental Condo on St Pete beach in Florida 2 years earlier, and was now about to buy a second one a little farther north. Mark was delighted I was interested in learning about them, and was only too eager to teach. In a flash he had a stack of pictures of his wife and kids playing in the sand and Ocean in front of his condo.

He related how he had purchased the unit 2 years ago, and managed to spend most all of our generous General Motors 4 weeks of vacation there on the Beach each year, for free. Here briefly was what I learned from Mark

The Basics of Vacation Rental Condos - The Overview

As Mark explained, the value of beachfront property has been growing steadily in Florida for many years. Almost since they finished construction of the Interstate Highway System in the US, more and more people have been traveling to Florida to spend a week or two on the beach for their summer vacation.

Additionally, many more retired couples spend their whole winters in Florida's warm climate. And surprisingly, Europeans enjoy traveling to Florida in the Fall (for some of Florida's best weather). So the result is that Florida Beaches have become a very popular year round travel destination

That was no secret to me, I explained to Mark, we take our kids to Florida for Summer vacations and to spend a day at Disney, so I know you're right, and it does cost us a mint to stay directly on the beach at St. Pete.

"Right" replied Mark, "and probably you're staying in a cramped one room, 2 bed, beach motel where the kids drive you nuts and make relaxing impossible". Right again. "So wouldn't you rather stay in one of my 1,000 sq feet, 2 bedroom, 2 bath beach front condos with a full living room and kitchen, for about the same amount of money?"

(And of course that's exactly what I did the following year, but I'm getting ahead of the story).

"But Mark", I asked, "how can you possibility own and rent a place all the way down in Florida when you live up here in Michigan"?

Mark went on to explain the "Vacation Rental Condo" he owned had an "On-Site Rental Office"." It's almost like a hotel. It's got a Rental Office that is open 6 days a week, there's a staff of 2. They rent my unit for me, arrange for the cleaning and maintenance, handle all of the problems, and mail me a check once a month. Whenever it's not rented, and I can get the time off, we spend some great FREE vacation time there".

But as mark explained, he didn't buy it simply to take vacations, he enjoyed traveling all over, he bought it for a retirement investment. Mark explained how this Vacation Rental unit was very expensive (if I remember correctly somewhere in the neighborhood of 3 times more than the home he lived in), but he had some savings he'd managed to put away toward retirement over the years, enough for a down payment, and was able to get a mortgage for the rest.

So do you get enough rental income to make the mortgage payments", I asked.

"No way", Mark explained

"Well that doesn't seem to be a very good investment, does it?", I asked

"That's because you're not looking at the big picture", Mark Said, "Try to think about it like this:"

"So far in my life, the best investment I have made has been in my home. The value of my home has almost doubled in the last seven years. I simply cannot save money as fast as my investment in my home is generating money for me. I would love to invest in another home and double the amount of value it is generating, but I simply could not afford payments on a second home".

"But what if you rented out the second home, wouldn't that be the same as owning a Rental Condo in Florida (that you also couldn't afford)", I joked.

"No, it's not", Mark reminded me, "when you rent out a home you're doing long-term rentals, you're just asking for problems", I thought you knew all about that".

(Mark was so right; when I owned the small apartment building I learned all the pitfalls. Mark patiently started outlining a list as we talked, comparing the difference between owning Residential Apartments (or Single Family Homes) vs. Vacation Rentals).

Mark was explaining, OK, so you do understand that there are some advantages in investing in Real Estate, right? But there many different types of Real Estate that one could invest in. "When you rent out a single family home or residential apartment you're doing long-term rentals, you're just asking for problems". Mark patiently drew up the following list as we talked, comparing the difference between owning Rental Homes/Apartments vs. Vacation Rentals).

Advantages of owning Rental property - a Single Family Rental Home or small Apartment Building

• It is a method of building wealth by utilizing other people's money to acquire an income producing, appreciating asset

• Property appreciates on average 3-5 % per year (or more) building wealth for you when you sell it

• Generates (a small) yearly Income Tax savings

• Rental income helps you make the mortgage payments

• Rental Income grows over the years while the mortgage payment stays the same (usually the investment will have a negative cash flow (yearly loss) over the early years of ownership, but later start breaking even. Eventually it will be profitable each year, in addition to growing in value each year through appreciation)

DIS-Advantages of owning Rental property - a Single Family Rental Home or small Apartment Building

• The sad fact, bluntly put: many home or apartment renters are losers and liars

• Tenants quit paying their rent or bounce checks

• It is expensive and time consuming to evict bad tenants, it may be personally intimidating.

• Un-wed mothers with children are almost impossible to evict - owner is the bad guy, countless months of lost rental income result

• Toxic tenants may fight eviction with legal help for months (or years!)

• Often the owner is directly involved managing, collecting, and evicting. (Not really fun) and may be personally intimidating.

Mark then started drawing up a chart for short-term Vacation Rental Rpoperties, as he pointed out that Vacation Rentals enjoy ALL of the advantages of Single Family Rental Homes or Small Apartment Buildings (that being that no one would buy or own them if there wasn't any economical reason to), but they share few if any) of the dis-advantages:

Advantages of owning Vacation Rental Properties - (Vacation Condo Units)

• It is a method of building wealth by utilizing other people's money to acquire an income producing, appreciating asset

• Unique Oceanfront Property appreciates above average 4-7 % per year (or more) building wealth for you when you sell it

• Generates (a small) yearly Income Tax savings

• Rental income helps you make the mortgage payments

• Rental Income grows over the years while the mortgage payment stays the same (usually the investment will have a negative cash flow (yearly loss) over the early years of ownership, but later start breaking even. Eventually it will be profitable each year, in addition to growing in value each year through appreciation)

• Raising Rental rates is easy (because every renter is "new") - you're not raising the rent on an existing tenant.

• Vacation Renters are Winners, they are in the top economic class able to afford to pay upwards of $1,000 to 2,000 PER WEEK

• Rentals are Short Term Vacation rentals - eviction virtually never happens - (They have to return to work or catch a plane)

• Vacation Rentals are usually fully paid in advance - no income loss - no bounced checks

• Often the owner is NOT directly involved managing, but lives in another state and simply gets rental income checks sent to him monthly - (fun!).

• The owner gets FREE vacation stays for his family and friends - (fun!).

• The owner gets pride of ownership; (bragging rights), believe it or not it is kind of fun to own Oceanfront properties! - (fun!).

"Gee all that sounds pretty good, but Mark, there must be some downside, right?"

DIS-Advantages of owning Vacation Rental Properties - (Vacation Condo Units)

• It is not as simple as putting money in the bank and collecting token interest.

• Initial work is involved; a suitable Vacation Rental must be located, purchased, and financed.

• There is yearly (minor) accounting and record keeping involved

• Depreciated properties are subject to Federal Tax "Recapture" at their sale

Mark finished our conversation by explaining how his Florida Vacation Rental properties would enhance his retirement

"Based upon my very conservative growth projections", Mark said, "by the time I retire in 12 to 14 years, my units should be worth almost a half million dollars each." "In other words, in addition to the appreciation in my Michigan home, and my GM Retirement, I'll have almost a million dollars of Florida proprieties." "Then I can perhaps retire to Florida and live in one unit on the Beach, and keep the other to increase my retirement income".

"Or maybe I'll sell one and build a new Golf Course Home inland, paying cash for it. Or who knows, maybe I'll sell both of them and move to California. I love the idea of retiring early, with enough wealth built up through my Real Estate investments to give me a interesting and well funded retirement".

"So what's your retirement plan?", asked Mark.

"Actually I haven't thought much about it", I replied, "but after listening to my Doctor, and now you, I'm not asking all these questions for nothing. Help me understand something, my home is the most expensive thing I own, just buying that home was pretty scary to me, and you're talking about buying something on the beach costing maybe 3 times more than the house I'm living in?"

"Suppose I found a nice Rental Condo inland, maybe around Orlando, for maybe $25,000, something more affordable, wouldn't that be a more realistic plan? I could rent it and also vacation in it when it was empty, and if the real estate was appreciating at say 8% a year in Florida, it would also appreciate the same amount, right?"

Leverage

"There's so much wrong with that idea I don't know where to begin, said Mark. Do you know about "Leverage"? Let's look at a simple example. Suppose you have saved $20,000, you could buy a $25,000 Vacation Rental unit or a $125,000 unit, which would you buy?"

"Conservative me would buy the $25,000 one and have small payments and sleep at night", I replied.

"Ok that's fine, but you do understand that after 8 years of appreciation, your $25,000 unit would be worth about $46,000, while the $125,000 one would be worth about $231,000. Put another way, for the same $20,000 investment you could make either

Invest $20,000 - ($46,000 - $25,000) = $21,000 profit

Invest $20,000 - ($231,000 - $ 125,000)= $106,000 profit

"Now before you jump all over me I know that comparison isn't fair, it's not counting your mortgage payments, said Mark, but it illustrates what leverage is. In other words, if everything is appreciating by 6% (or 8%, or whatever), the more expensive place you own, the more profit you will make. So the general rule is to purchase the most expensive Vacation Rental unit you can".

"But Mark, I couldn't afford to make the payments on a place costing 3 times as much as my home", I replied, how can you do it?"

"You'd be surprised, said Mark, remember the rental income is going to help you with the payments on the expensive unit, in effect, those renters will be helping you buy it. On your lower cost unit, you'll get virtually no help with the payments because no one will want to rent it". Florida is absolutely full of low cost (empty) condo units, even on golf courses, only really desirable prime waterfront units really work well as Vacation Rentals".

"And yes, it will probably require a little sacrifice in the short term, to make those additional mortgage payments. I do it by using some of the funds I would normally be saving in an IRA or retirement fund. I figure since I'm investing in the Vacation Rental unit for my retirement, the money's going to a good purpose".

"Look, it's like this, some people live for the moment, spending all their income on expensive cars, clothes, travel; acting like they're rich, when in reality they're just pissing away their future paying credit card interest! They may not realize it yet, but sooner (likely later), it will dawn on them that they will never really be able to retire and enjoy life, but will be forced to still be working when they're 60 or 70 years old. Ever notice those old men bagging your groceries? Think they're still working for the fun of it?"

"No, I know what you mean, I replied, I fully invest in our 401k plan and have mutual fund IRA's as well. I also want to retire young, and have as many years as possible living the free life where I'm not chained to a job, and all my time is my own. And since my 401k and other investments are not doing much for me lately, I'm really interested in learning more about this Vacation Rental stuff".

"So Mark, let me ask you one more thing, a friend of mine recently purchased a Time Share Vacation unit in Florida which he can rent out while he's not using it, and it didn't cost anything like you're talking about," I asked, "so wouldn't that be an easy way to start getting into Vacation Rental investments?"

***********************

Chapter 3 - What is a "Vacation Rental" (NOT A TIMESHARE!)

***********************

"Oh my God, replied Mark, you haven't heard a thing I've been telling you!"

"Sorry Mark, but I guess I'm not really sure what the difference is between a Timeshare and what you're talking about", I replied.

"Wow", said mark, "I just assumed that by now everyone in the world knew what a terrible investment a Timeshare is! You should spend some time learning about them on your own, I can just give you an overview".

"Think of it like this, for all practical purposes, "timeshare owners" are simply renters who have signed-up for a life-time lease, that they are stuck with for eternity!"

"When you buy a Timeshare you really are not purchasing a tangible asset like a piece of property, you are only purchasing the right to spend a set period of time each year in a property owned by someone else!", said Mark.

"Actually you don't get ownership of any physical thing when your purchase a timeshare, you only get the legal right to stay a week (or whatever length you purchase). Along with that right comes the responsibility to pay all the monthly and yearly fees associated with ownership. You have virtually no input to what happens to the property over the years because again, you don't own the property".

"Contrary to what they tell you, fees and expenses will increase over the years, and you are legally bound to keep paying, whether you use it or not . The real problem with timeshares comes when you tire of it and try to sell it, it's usually only then that "owners" realize there are virtually no buyers. Not only is there seldom any appreciation on a timeshare, but it's not uncommon for older timeshares to sell for half or less of their original cost! No matter how you look at, a timeshare is clearly not "an appreciating asset".

"Unfortunately, often the only way timeshare owners can get out from under their investment is to give it away FOR FREE to some charity for a slight tax loss".

But all this totally misses the point, what I'm talking about is a secure real estate property investment, not a vacation, it just so happens that when you purchase a Vacation Rental Condo, you own it, and of course may stay in it "on vacation" anytime you wish.

"Let's see if I can draw up a short list of the difference between a Timeshare and the type of "Vacation Rental" I'm talking about".

"Vacation Rentals" (what Mark is talking about)

Let me pause a minute to define terms. The subject of this book is a wholly owned domicile or vacation home, that is often located in a resort area, and whose primary purpose may be to generate revenue through short-term rentals. For the purposes of this book, the term "Vacation Rental" may apply equally to either a stand-alone home or an individual unit in a larger condominium.

Understand that "Vacation Rental" is not a standard type of real estate property per se, but simply a general term that may be applied to any home or condominium unit that happens to be in a desirable vacation destination and has certain enabling properties (chiefly, the legal ability to be rented short-term).

A Vacation Rental is a serious, expensive real estate investment, exactly like purchasing a home. You usually get a regular mortgage to finance it, you have a closing (or) settlement, you will get a deed, and you own the Vacation Rental Property. In effect, you can think of it as owning a 2nd home or Vacation Home, it's all yours!

A Vacation Rental is an expensive piece of real estate. (In 2007 costs) - from $200,000 to $1,000,000 or more. Usually only purchased by individuals (or partners) who already have enough savings to be able to make a reasonable down payment, enjoy an good credit rating to obtain a mortgage, and (like any new business), have enough additional income or savings to "carry" their new investment some years until it achieves positive cash flow

Timeshare (or) Vacation Timeshare (or) Interval Ownership Vacation (or) Fractional Ownership (or) 100 other names

A Vacation Rental is not a "timeshare" or anything like it. A "Timeshare" (or any of the above named entities), is a relatively inexpensive (2007 costs - from $5,000 up to $35,000 or more) non-real estate "investment". I say "non-real estate" since while there will certainly be a beautiful resort complex involved; you won't actually own any part of it (except its bills)! And I use the term "investment" very loosely, as thousands of Timeshare "owners" have learned the hard way over the years

Tens of thousands of people who purchased Timeshares have found they cannot sell them (and are tired of the endless scams from businesses who promise them they can sell them for an up-front fee).

"The key is, If someone is giving you a "free vacation", a "free cruise", or simply a "free lunch", to come and learn about their new Vacation Ownership - it is a "Timeshare"! Please understand that you will not be purchasing the type of appreciating real estate investment that I am talking about", said Mark.

***********************

Chapter 4 - The Search and Purchase of my 1st Vacation Rental

***********************

Over the following year, I had many discussions with Mark concerning his Rental Units. Finally I planned a driving trip to Florida to see first hand what this investment was all about. Mark gave me directions to his unit (which was rented at the time), but I visited it down in St Pete and was able to see that it was an attractive place, was directly across the street from the beach, and apparently had a great Gulf View.

I actually spent the better part of 2 weeks driving around the coastline of Florida, looking at both the East Coast (on the Atlantic Ocean), and the West Coast (on the Gulf of Mexico). By now I was picking up the free Real Estate Books that are on every corner and starting to learn about what to look for. In general, based upon what Mark had taught me, I was looking for a beachfront unit (either across the street from the beach, or directly on the beach). I wanted a "great Ocean View". (I learned that even though all of the West Coast units are actually on the "Gulf of Mexico", they called them "oceanfront"!

I wanted a complex that had an "on-site" Rental Office, (although later I learned that that wasn't so important as every beach community has many independent Rental Offices that handle Rental Units for out of state owners). I thought I wanted something that was "almost new", something that didn't need any work, something that was fresh and new. Boy was I in for a surprise.

Florida Beaches

Probably the first thing I realized was that I had always pictured the whole state of Florida as surrounded by beautiful sandy beaches, and assumed that down at the bottom (Key West), would have the best beaches. I quickly learned that the whole "Florida Keys" (including Key West), has almost no beaches, only tiny man-made beaches. In general that whole area has a rockey coral crusted coastline. There are plenty of rentals, but very few Beach Rentals of the type I was looking for.

Mark had cautioned me that a successful Vacation Rental had to be located somewhere where it is relatively warm year round. According to Mark (and later confirmed by me), that "upper limit" in Florida is a horizontal line passing through Tampa Bay. Looking at a Florida map, picture a line going right through Tampa Bay. In the winter, communities above that line will sometimes get down to freezing during cold spells, while cities south of Tampa will stay relatively warm.

Another big factor was "East Coast" vs. "West Coast". In prior years I had stayed in Daytona Beach (East Coast), but knew from experience it often gets freezing there in the winter months. Also, often the Atlantic Ocean could look pretty rough, gray, cloudy, and sometimes seemingly dirty. Also, silly as this may sound, you couldn't watch a beautiful sunset (only sunrises). One day while driving across Florida, East to West, I happened to listen to a talk-show who's main subject was, which Florida coast is better?

Florida Coasts - East Coast vs. West Coast

Of course this is an impossible question as there is no single answer that everyone could agree on, but I did learn much valuable information. For example, the East Coast is much more populated than the West Coast, with many of the residents coming from the Eastern US, New York and New jersey, etc. I learned there are more highways, more cities, and more traffic on the East Coast

Supporters of the West Coast argued that the weather is better on the West Coast, warmer in the winter months, and overall does not rain as much. (Having now lived here in Florida I can confirm that that is true). West Coasters maintained their population is mostly made up of mid-western folks, kinder and gentler, and more laid back and easy going. And figures seem to confirm that there is less crime on the West Coast

But as I said, I had vacationed in the summer in St Pete and Treasure Island (West Coast, by St. Pete), as well as Daytona Beach (East Coast) , and already knew in my heart that I also preferred the West Coast, with its fabulous beaches, turquoise water, and golden sunsets! So I focused upon visiting every beach community between Tampa Bay (didn't want anything up in the colder area), and the "bottom" of Florida, Marco Island, searching specifically for Rental Condos, and considering the overall beach community.

I looked heavily in the many beach communities around Tampa bay starting with the first real beach on the lower West Coast of Florida (Clearwater Beach), and working my way on down through Treasure Island, Belleair, Indian Shores, Redington, Madeira, Treasure, and Saint Petersburg Beaches. I was quickly learning that I was not finding any new (or even newer) Rental Condos, only older ones. And actually many of them looked pretty rough. Also, some of the neighborhoods also looked rough. Some areas looked very commercial, although they also looked like fun places to vacation!

The Elusive Vacation Rental Condo

But overall I was learning that the various beachfront buildings could be divided into Hotels, Motels, Timeshares, Residential Condominiums (full-time residents that do not allow short-term rentals), and very - very few "Vacation Rental Condos" that I had learned so much about from Mark. I was starting to learn that like everything in life, there is a catch. I learned that even if I had all the money in the world I would not find one brand new, beachfront, short-term vacation rental condo, there simply wasn't any new ones being built. I came to realize the obvious, that all the really best Florida beach property had been built up many years ago, and finding a "new" Rental Condo would be almost impossible. Oh well I figured, I couldn't afford a brand new one anyway, so I started changing my focus to look for "newer" units still in good condition.

Traveling south, the next group of beaches are Anna Marie Island, Holmes and Bradenton Beaches. While they are all different, there are remarkably few beachfront units of any kind directly on the beach, and only a few Vacation Rental Condos

Longboat, Lido, Siesta, and Casey Keys

Continuing south, I found the next group of Florida offshore barrier islands, called "Keys" (Not to be confused with the Florida Keys, south of Miami). I instantly fell in love with Longboat Key, a lush green, very private and very non-commercial island. Longboat is worlds apart from anything I'd seen up till then, clearly a high class, very exclusive island. I thought I had found my perfect Florida location (of course you surely know the main Real Estate rule #1, "It's all about Location, Location, Location"). And clearly, Longboat Key was a perfect vacation location!

But I was running out of time on my initial search of the lower Gulf Coast, so I finished up with Lido Key, just south of Longboat, before heading back to cold Detroit. Just as I left the Key, I packed the van with free Real Estate books to add to my growing collection.

More Florida Trips

Back in the shop, I shared my adventure with Mark, and was somewhat surprised to learn that he didn't know anything about the beaches south of his St Pete location. So now, I was becoming the teacher and Mark was interested in learning all about my trip. I confessed that as much as I liked the St. Pete area, I thought I liked the Sarasota, Longboat Key area better, but had to admit that I had not had enough time to really shop for Vacation Rental Condos.

In later trips, I visited Venice, Punta Gorda, Fort Meyers, Naples, and Marco Island, completing my lower West Coast survey. I collected hundreds of Real Estate handouts, followed up on newspaper ads, and cruised beach neighborhoods, and (at least in my own mind), became very knowledgeable of the most desirable locations for vacationers that also had some Vacation Rental Condos for sale. Now that my search was over, it was time to focus on a specific area and try to locate a good used Rental Condo to purchase and get started.

Discovering Siesta Key

Now that I had completed the initial scouting of Florida, it was time to get the wife involved. I was all ready to make a purchase offer on a Vacation Rental Condo on Longboat Key named "Sand Cay" (still a very viable direct ocean front condo complex). I had found a setback unit with a tiny "partial ocean view", but a relatively affordable price, and it had a reasonable rental history. The wife wasn't convinced however that this was the place to invest our hard earned life savings

Her logic was simple, if we're "going for broke", let's go all the way and get something closer to the front, with a full ocean view. It was not that I wasn't interested in this myself, it was simply that there wasn't any units closer to the ocean currently for sale and I was told, when they do come up occasionally for sale, they ask top dollar for them.

"What about this Siesta Key", said the wife, "what's for sale down there?"

"Actually I never quite made it down there yet", I replied. It was true. Once I discovered Longboat Key, I was sure there couldn't possibility be anything better on the West Coast of Florida. I was blinded by Longboat's lush green golf courses, world-class reputation, and beautiful beach! I already pictured myself walking its tropical shores, toasting the sunsets, and basking in the good life of its rich Country Club attitude

As we crossed the bridge onto Siesta Key for the first time, I immediately knew that even though it was only 20 minutes south of Longboat, it was light years away in appearance. The road was much narrower and surrounded by a rich tropical forest; it immediately seemed more primitive and jungle-like. And it seemed like every other home or condo was for sale! (Later I learned that is because there's lots of investors who buy something, tack a few 100k on the price, and put it right back on the market).

Siesta Key Village

Soon we ended up in a quaint little shopping / restaurant area I learned was "Siesta Village", with outdoor dinning, Ice Cream Shops, and a very touristy atmosphere I learned later made Siesta Key desirable by many folks as a fun vacation area! As I learned that day, Siesta has a Island style, laid back feeling that can't be touched by Longboat, or any other vacation spot on the West Coast of Florida.

We ended up "shopping" for "Rental Condos" while all the tourists were shopping for trinkets! We drove along the Main street (Midnight Pass rd.), where Condo after Condo sat directly on the Gulf of Mexico. We stopped at each place that had a rental office, and while tourists were looking for a place to rent, we were drawing up charts of each place using the tips Mark had taught me to look for, do you have 1 week rentals? Do you have full Ocean Views? Are any units currently "For Sale"?

After a full day of this we were learning the usual, that there were few really super desirable "Vacation Rental" condos for sale at that time, most were either farther back (with "peek-a-boo" views), "across the street from the beach", or had no view, or were really old, rundown "dumps". (Later we learned that we could have bought almost anything on Siesta Key and still made out great).

Lucky Lunch

By this time we were down by the second commercial area of Siesta Key called "South Bridge Shops", so we stopped for lunch at "City Pizza" (still there) and to discuss our flight home, leaving that evening

Next door to the pizza place was a real estate office with Real Estate books outside, so I grabbed one to study during lunch. There was a sign in the window of the real estate office that said something like, "if you're looking for Vacation Rental investments on Siesta Key", call Pam. "I know which condos have the best rental programs, which ones allow daily, weekly, or monthly rentals, and which have the strongest condo associations, best reserves, and future assessments. I can get 90% financing, even for investments!"

A quick check in the office revealed Pam wasn't there, so I left a message. A half hour later, in the middle of lunch, in walks Pam, who looks around and spots us as the only likely tourists shopping for investments.

The "Pocket Listing"

We instantly liked Pam's positive nature and in-depth knowledge of everything for sale on Siesta Key. More importantly, she was an investor herself, and had all the "inside knowledge" and connections that would prove so valuable.

We explained our frustration at not really being able to find a really great direct oceanfront unit, opposed to the fair number that were way back with little or no views. Pam explained that it is true that often the most desirable units are so valuable that owners tend to leave them in the family, selling them to relatives, or in some cases sell them to other owners in the same Condo Association (that own units farther back from the ocean and want to move up).

Then Pam remembered a "pocket listing" she had from one of her clients at "Island House". (As we learned, apocket listing means that the owner doesn't want to list it actively for sale, but has expressed an interest in possibility selling his property if the price was right). Within a few minutes, Pam had arranged for us to take a look at it. (It was only about 6 blocks away, Siesta Key being a relatively small island). It was Love / Hate at first sight! As Pam said, it was in the front building of a condominium called "Island House", directly on "Crescent Beach" (Also called Siesta Key Beach). Better yet it was on the ground floor, with a door on the Lanai (Florida talk for "front porch"), right to the beach.

It was also ugly as hell on the outside. It looked like an old airplane hanger (because all the windows were covered with corrugated aluminum storm shutters). The inside was large and ancient, looking dimly like a 1940's funeral parlor (and smelling about the same). Since all the windows were covered, it was dark inside, and impossible to see the "view".

The most striking feature was the green jungle-plant wallpaper that covered the complete kitchen, including the ceiling! The olive green appliances took me back to the 60's. While it was pretty much a turnoff, I still couldn't deny it's direct Gulf front location (and clearly it would have a "killer" ocean view, when the storm panels were removed).

Even though we were beginners in this game, all my "homework" of shopping and looking at other units told me this was a rare and desirable investment. Pam assured us that while this unit had not been in the rental program, other comparable units in "Island House" brought in $20,000 - $25,000 yearly. After a nerve-shattering hour of discussion, and with the added pressure of having to leave to catch a flight, we offered something like $265,000 on the asking price of $285,000, and flew back to gray cold Michigan.

Sealing the Deal - Long Distance

Clearly it would have been almost impossible to purchase this investment without a professional Real Estate persons help. During the next action packed week at home, we talked to Pam daily. I also spent hours going over the finances. I knew if I removed some of my retirement savings, I could swing a down payment. And we had enough additional savings to afford to do a very modest upgrade of the interior. We would hire someone to replace the kitchen cabinets and countertops, and do some painting and other chores ourselves.

I spent hours creating spreadsheets trying to determine how much our yearly expenses would be, and how much possible income we might get. I pretty much figured that (after the improvements), and renting it as much as possible, we would fall short of our total yearly expenses by about $5,000 - $8,000 per year. I rationalized that we'd save half of that by utilizing it for our vacations, so it looked do able. Scary - but not impossible.

And on those spreadsheets I figured modest increases in rent income, and appreciation in the property value would make it "break even" on paper in a few years

The Final Decision

As it turned out, the owner (a used-car dealership owner from Illinois), wouldn't take anything under his asking price, so he rejected our offer. But by now I knew this unit had everything we were looking for. (And after my months long learning curve of surveying thousands of Florida Vacation Rentals I new what I was looking for, and realized that the really good investment units are somewhat rare), so I knew this unit was a diamond in the rough

Our logic was simple. This was a rare ground floor, front building unit, with killer Gulf Views. It had all the important features we were looking for in a Vacation Rental including a very active on-site Rental Office, a very reasonable management fee of 15% (In other words the Rental Office will rent and manage the unit and send us monthly checks, for 15% of the gross), and a magnificent crystal white sandy beach that we would love to vacation on with family and friends.

Another thing that made me feel that it had to be a good investment was the fact that the president of the Condo Association owned 3 units himself! I learned that virtually every Board member owned more than one unit. (And not that it mattered, but many of the Board members were from Michigan).

Once our "list price" offer was accepted, we started seriously planning our next trip down to Florida (the closing), and how to best utilize our time planning the improvements we wanted to immediately make

The Closing Adventure

A month or so later we flew back down to Florida to close on the property, bringing old friends to celebrate with us (party time!). By then the place was empty (the previous owner had removed all his antique furniture (saving us the trouble of scraping it)). The Condo Association had removed the "Hurricane Shutters" and that opened up a glorious full gulf view from our unit

That first day we bought new mattresses and laid them on the floor to sleep - (The girls had brought down linens). Ya, we were roughing it, but what a exciting time it was - the biggest expensive we had ever taken on in our whole life was also the most exciting thing we'd ever done!

We learned the names of local modernization contractors (and also learned that Florida wages for this kind of work are very reasonable compared to Detroit's trade union wage scale). We settled on "Tom", a local guy who showed us other units in our same complex he had already remodeled. We decided on some very minimum changes, inexpensive Formica countertops and white plastic cabinets.

With those 1992 prices, the whole job cost us about $9,000. The girls busied themselves with shopping at "Goodwill", finding incredible furniture bargains, day after day. In a very short time the place looked "decent", and of course, the Gulf beach and view was to die for.

***********************

Chapter 5 - The Ongoing Adventure of Ownership

***********************

The excitement continued back in Michigan as the first monthly rental checks started coming in. In those first years, we rented our unit as much as possible, which was about 60-70% of the year, but that still left us months of time to use it ourselves, or to let our friends use it even if we couldn't come down ourselves.

We just couldn't stand to see an empty week when we knew some of our friends or relatives who had vacation time would love to use it, so we always encouraged them to. We'd only ask them to pay for a few expenses like part of the electric bill (for their air conditioning), or whatever, and they would always be more than generous back to us.

During most of the 90's we spent every Thanksgiving and every Christmas Holiday there with our children and extended family. Additionally we did golfing weeks or weekends, always getting as much use as possible out of our unit. We found all the air bargains and often could do the round trip for $140 or so. I perfected the Detroit-Sarasota "one day" driving trip. (Roll out of the motor city at 4am and roll into Siesta Key in time for Johnny Carson!). During those years I really couldn't understand why anyone would waste 2 whole days driving to Florida when it only required one day!

Appreciating Property

We were enjoying the ownership of our "piece of paradise" so much in those days, we really didn't pay too much attention to its appreciating value at first. We stayed in touch with Pam, and every year or so she would call to say she had a buyer if we were ready to sell for a really nice profit. But selling was the last thing on our mind. We knew how much prep work it had taken to discover "Siesta Key", and this ideal Vacation Rental unit, and couldn't see any sense in giving it up.

Still it was exciting to listen to offers. Consider that we originally put about $65,000 up for a downpayment, and then maybe another $15,000 to get it ready to rent, and maybe about $8,000 more per year to carry its expenses. So after 3-4 years or so, we had about $100,000 invested in total. Pam would call saying she could get us like $475,000 for it. I'd quickly figure we had roughly a $220,000 mortgage, so we could walk away with about $140,000 profit on our $100,000 investment - well over doubling our money in just 4 years or so!

A couple things were happening. While I didn't consider it initially, our Vacation Rental investment was kind of aforced savings plan. The yearly extra money we were adding to cover the expenses - we would clearly get all back! - every penny! For example, if we had sold it for about $475,000 back then, after the mortgage was paid off, we would have walked away with about $255,000 in our pockets (not counting the selling commission). The point is, it wasn't like it was "costing us" $8,000 a year to own it, it actually was forcing us to save $8,000 per year (which we would get all back when we sold it).

Of course it didn't continue to cost us $8,000 per year to carry it, rents went up 5% to 10% yearly and it started breaking even or making a small yearly profit.

Thinking Retirement

About that time I started thinking more seriously about my retirement. Funny when you're in your 20s, 30s, or even 40's, retirement seems so far away that you cannot even imagine you'll ever get there and so why think about it? But the reality is on average, you certainly will reach retirement, and you may have many many years of it!

I'd had a great model for retirement, my dad! My dad (an accountant at GM), had a simple retirement goal, structure your life so that you're able to spend the same number of years not working, as you did working!

It seemed like a good plan if you could accomplish it. (My dad almost did. He worked some 30+ years at GM and took an early retirement at about 55, then enjoyed almost 30 years of retirement in a South Carolina Golf Community). (Note the desire to escape from Michigan)!

But I never "got" Golf, and I also knew I didn't want to work up to the day I died on the same relatively boring job at GM, but wanted instead to get out into the world, try new things, and have time and money to enjoy (hopefully) a long and richly rewarding retirement.

It was becoming clear to me that my Vacation Rental investment on Siesta Key was appreciating and making money for me much more rapidly (and safely) than my 401K plan at work was doing. I was seeing that I'd be better off taking whatever other money I could get my hands on and buying another unit on Siesta Key. By then I was seeing that Siesta Key property was not only something I could invest in, but was something I was really interested in learning more about and pursuing as an activity that I would enjoy doing part time in retirement

Additional Vacation Rental Investments

I am not going to waste your time describing my additional Vacation Rental investments that I have made here on Siesta Key (where I now live in retirement, looking down on the turquoise waters of the Gulf), and spend my time playing with website design, vacation rentals, property investments, and whatever other interesting (to me) activity I chose.

But after our Island House unit over doubled in value, and it's yearly rental income doubled, we were left with the nice problem of having a great deal of equity built up, so what to do with it? Buy more Vacation Rentals of course. And that's just what we did. (Kind of a "Mini-Donald Trump" play).

So around 1998 we purchased a second VR (Vacation Rental), and about 2000, we acquired our third one, right here on what has to be one of the very best VR investment areas in the world. (At least that's what my renters who come from all over the world tell me).

And as I write this (2007), both those newer additions have more than doubled in value, while the original Island House investment has (how do you spell it) QUADRUPLED in value! And they all just continued to appreciate while generating increasingly income.

Unsustainable Growth rate

Since Siesta Key was basically completely "built out" 30 years ago, there is virtually no beach front (or) bayfront property available to build anything new on. So visitors and investors discovering Siesta Key and desiring to own a piece of us continued to drive the appreciation until it finally became unsustainable.

All during the 90's, we enjoyed a moderate growth rate that assured continued price escalation on virtually any property on the island one would purchase. As I purchased additional units I would study competitive properties at length, making spreadsheets, shooting videos, trying to determine the very best investment. As it turned out, every single unit I considered purchasing, I should have! Not only did everything we purchase turn out a winner, but everything we didn't buy turned out a winner for someone else

As Internet use grew, more and more people from all over the world, started discovering Siesta Key. And once they visited, usually they became converts, returning year after year for our incredible beaches and weather. Property values continued to increase until they were averaging 14% to 16% per year in the early 2000's! For a while it resembled San Francisco or other West Coast growth rates that just continued to spiral. Unfortunately for us (as well as the rest of the U.S. and actually the whole World), we were heading toward having the 2nd worst recession in our history!!

***********************

Chapter 6 - The Real Estate Bubble and Meltdown

***********************

They say the peak happened in 2005-6, when prices finally paused to take a breath, and inventory began to accumulate. Just so you can get a perspective, in 2005, ocean front units in Island House were listed at $1,450,000 to $1,750,000 and a few actually sold close to their asking prices.

All of a sudden in fall 2005, it seemed all the buyers and investors just gave up and went "on strike", deciding to wait until prices came back to "normal". In 2006, real estate sales stayed very flat while inventories continued to build. I've read that during the peak there were only 50 or so properties on our market, now there were more like 450!

All the newspapers were talking about the Real Estate Bubble Bursting. More enlightened articles examined the fact that there is really no such thing as a single national real estate market, only many local markets. And while they may all slightly trend together, individual markets (Like San Francisco) move entirely different than say, Detroit!

All during 2007 and partway into 2008, Siesta Key prices continued in their negative direction. Direct Beachfront units that in previous years were virtually impossible to find, now started to appear and at substantial discounts from only a few years ago. It was depressing to watch the paper values I had built up in my mini Vacation Rental Empire tanking! We all started talking about the "years when we used to be rich!" (However things were not really that bad here on the Key!)

As bad as it was getting all over Florida, it continued to be clear that prime ocean front condos on Siesta Key were suffering considerable less than (for example) 3 bedroom mainland homes. While they did lose perhaps 25%-35% of their previous (highly inflated) values, many of us almost had feelings of relief. We knew that our real estate values were finally undergoing the long awaited correction that was inevitable.

My guess is the Siesta Key real estate hit bottom in the fall of 2008. By January 2009, there were signs that sales were picking up all around Sarasota. Of course a main factor driving the increased sales were "pre-foreclosure" and Bank owned properties selling for considerable discounts.

As I pen this (April, 2009) investors are starting to creep into the marketplace, picking up deals that were unmatchable a few years back

Weathering the meltdown!!

The most surprising thing to me was there was no letdown on my Vacation Rentals. In fact my rentals have remained very constant for many years now , with increased grosses, caused by rental increases.

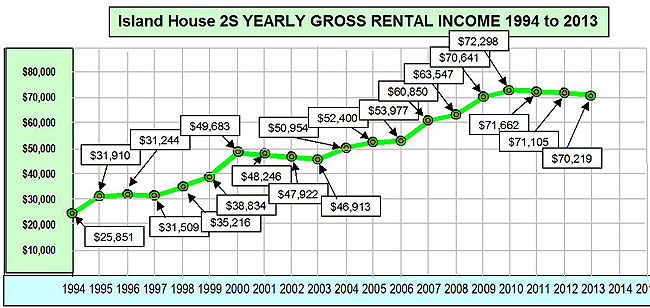

Sometimes a picture is worth a thousand words. Take a minute to carefully review the following chart, which depicts the actual rental gross income I have received over the past 20 years of ownership of my original Vacation Rental unit (Unit 2 South, in Island House on Siesta Key).

What is most impressive is the fact that during the worst years of our recent 2008 Recession (using whatever years you think it was the worst), the Vacation Rental income from this single unit not only didn't tank, it GREW!

This is clear evidence supporting the fact that not only is Siesta Key an almost recession-proof vacation venue, but also quality Vacation Rentals are very sound long-term investments!

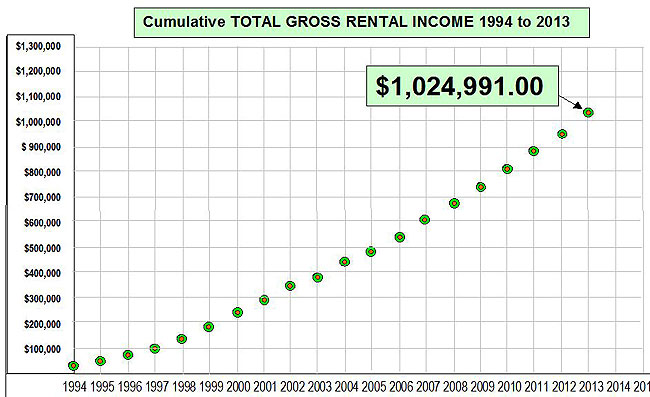

This next chart illustrates the cumulative GROSS RENTAL INCOME that that single unit has created over the last 20 years of ownership. Enough to pay for itself! (Remember its original cost (top-price at that time)) was $285,000.

Leverage (Remember?)

Here's another part of this story that is often overlooked by casual readers who don't fully grasp the Real Estate concept of "Leverage".

At some point we investors will sell our Vacation Rental units to realize our profits. While I will not speculate what price I could currently get for this rental property, it is fact that at one point (when a unit behind it sold for $1,375,000), that its value was well over a million dollars. (And it's pretty clear to me that as real estate values are once again climbing at a healthy rate both in the U.S., and here on Siesta Key), that it will easily top a million in perhaps as soon as 2-3 years or so?

But being the conservative investor that I am, let's say I can only get about $885,000 for it. (And yes - I will have to pay some taxes on my profit - but I'm always OK with paying taxes because you have to have PROFITS in order to qualify).

My point is if one is not paying attention, one may be thinking, OK you bought it for $285,000 and sold it for $885,000, so you made a fair (but not outstanding profit - after all it took 20 years to grow to $885,000.

(And that would be correct)

Except that I didn't actually pay $285,000 for it, I only paid the initial $65,000 down payment, and then an additional $30,000 - $40,000 or so additional funds over the years to make up for the shortfall in mortgage payments - remember?

***********************

Chapter 7 - But is it, "TOO LATE BABY"?

***********************

OK, so no one can predict the future. By that fact it is impossible to predict if it is too late to get involved in Vacation Rental investments, but the very history of our country is a pretty strong indicator that in the "long-term", Real Estate (along with every other financial investment) will continue to increase in value

I remember purchasing my first home in the early sixties, a new 4 bedroom home with family room and (optional) fireplace for $17,200 (BRAND NEW!). Honest! (Of course my Dad couldn't believe a house could cost that much, as his first home cost somewhere under $3,000 in the 1940's).

After 6-8 years, I sold that 1st home for about double ($38,000), making enough profit to buy a $65,000 home. Some years later I sold it for double ($130,000) and used that profit for a down payment on an even more expensive home.

But of course after the massive Real Estate "Correction" of 2007-8, many home prices fell almost in half. So one is left with the thought that Yes, Real Estate Values will likely increase with the economy over the LONG-TERM, but with any investment, short-terms will always be risky

My research on the Internet (By the way: zillow.com is a really helpful resource), indicates that Florida Real Estate (including Vacation Rental Condos) bottomed out in value about 2010-2011 and are now once again growing at a more sustainable rate (like the old days, prior to the Real Estate Bubble)!

This is good news for anyone considering an investment in a Vacation Rental; it's simply a great time to jump in! It will still be more difficult to obtain a mortgage on a "Second Home" than it was during the crazy bubble years, but lately (July 2014), the newspapers are full of stories that they are "loosing-up" the rules for obtaining mortgages after the extreme tightening after the bubble!

(By the way, that is my first TIP on getting involved in Vacation Rentals), that is, when going for a mortgage, probably describe your property as a "2nd home", unfortunately as far as I know, there are no specific mortgage types for "Vacation Rentals", and likely your mortgage broker will not want to get involved in anything out of the ordinary.

But let's not jump ahead here, I only have two more subjects to cover that I think you will find accurate and helpful in searching for your perfect Vacation Rental. The next Chapter focuses on what you need to consider prior to purchasing something, and the last chapter (Really the most FUN - don't miss it), describes Hard Lessons learned from the Real Estate Bubble - really, you may want to skip to that now, it is not going to tell you what you think it will!

***********************

Chapter 8 - Considerations When Purchasing a Vacation Rental

***********************

In my 20 some years buying and selling (and managing) Vacation Rentals, I continue to be astounded by folks "looking for a nice Vacation Home for their families that they can rent when they're not there". The typical couple will know almost nothing about what is really important for them to know, and will rely exclusively on their Real Estate agent to help them.

The problem with this is, as necessary and helpful as the Real Estate Agents are, their main focus is selling the property - (remember, it is the seller that is paying them, not the purchaser.). That means is they are very careful in their discussions with you and they answer every question honestly. But it also means that (exactly like the advice your CPA gives you when your taxes are audited), they don't volunteer any additional information! This means it is really "buyer beware" when it comes to purchasing Vacation Rentals, you (the purchaser), better ask all the right questions (because your agent isn't going to risk losing a sale by telling you what questions you should be asking)!

The perfect example is, the couple finds a place, loves the unit and view, and asks if they can rent it when they are not using it. The typical Agent answer might be "sure, absolutely you can rent it". What will (of course) be missing will be all of the considerations regarding renting the unit. For example the agent will likely not tell you that your actual chance of renting it is practically nil. Why would your chances of renting be not very good? There are many reasons which I will review in this Chapter.

The Initial Consideration: Location, Location, and Location

This will always be everyone's initial consideration, where am I interested in owning a Vacation Rental property? Very often the answer will be in the place I most enjoy taking my vacations. (My experience was different because I had never heard of Siesta Key prior to finding it), but for many folks that question is already answered.

But if it's not already settled in your mind, it is helpful to know the locations most vacationers are looking for if your goal is an investment first. A few years ago I remember reading an interesting article concerning the type of vacation destination that is the most popular. Unfortunately I have not been able to find that source, but I remember that Beach vacations were by far the most popular, followed by Golf, Skiing, etc.

Cities are also very popular, some as a destination (Like San Francisco), and some because of their adjacent attractions, (Orlando, Disney). If your goal is maximum rental income, better consider a location that is desirable year-round

As the focus of this book is Siesta Key Vacation Rental properties, where we enjoy an almost year-round supply of clientele (Winter Snow-Birds, Spring Breakers, Family Summer Vacations, Fall European Visitors, and Holiday Guests), most of the information to follow will be focused on our tiny island!

Another unique characteristic of Siesta Key is that unlike most other Florida Beach communities, we have virtually NO BEACHFRONT HOTELS to compete with our privately owned Vacation Rentals. Depending upon exactly how you count buildings, we have approximately 50-60 Beachfront Condominiums, opposed to one "hotel-like" fractional ownership ("Timeshare") place.

So privately owned "Vacation Rentals" are the only game in town! (And possibility Siesta Key is the very best location in Florida to own one!)

Once your overall location is decided, the next consideration should be your planned usage

Focusing in on Florida Vacation Rentals, and more specifically Siesta Key beachfront locations, it becomes really important to understand exactly what your expectations are prior to searching for properties. While driving down "Midnight Pass" (our main street where all the beachfront condos are located), a visitor may think their main differences are in their architecture. But the reality is, their main differences are hidden in their "Association Documents" (Docs).

While it may seem strange to outsiders, the major differences between Siesta Key Condominium Complexes are their "Rental Rules", legally spelled out (and religiously policed), in their Docs. These rules are so very important for 2 reasons

(1.) They absolutely define the properties' personally! They clearly establish if a given complex is "Residential" or "Hotel" like.

(2.) They are "cast in stone" - the likelihood that the Rental Rules will ever change during one's ownership is extremely rare. (Read "Never").

Totally Residential Condominiums

Typically their Rental Rules call for a minimum rental of 2 or 3 months, meaning that short-term rentals are not possible. These Condominiums may get a one 2 or 3-month rental per year (in some years), or be leased for entire years (which is seldom profitable). Some of them also restrict rentals to only 1 or 2 per year in the docs. Some of these units are also restricted to "over 55 years old" owners only. Often renters must also be over 55. Clearly these units are not for a person looking for a profitable Vacation Rental, but like all Siesta Key properties, their values will appreciate over the long-term, and for the very private person who is not comfortable renting their investment, they may be perfect.

(Siesta Key Examples: Whisperings Sands, The Point)

Residential Condominiums

Typically their Rental Rules call for a minimum rental of 1 month, meaning that short-term rentals are not possible. These Condominiums will likely rent for 2-3 months during winter season, and in some cases an owner (of a particularly desirable unit) MAY get an additional summer and /or fall rental. Gross Annual Rentals could be from $18,000 to $28,000+. These units will appreciate over the long-term, and for the Vacation Rental owner, they may bring-in enough yearly income to cover many expenses like Condo Fees and Taxes, etc. , and yet allow the owner months and months of open time to enjoy their investment. (Of course if the owner plans on utilizing the unit their selves during the Peak winter season, most or all rental income will be lost.

(Siesta Key Examples: Gulf and Bay Club, Siesta Gulf View)

Residential-Vacation Rental Condominiums (Investor Compromise)

This is somewhat a "hybrid" on Siesta Key as there are only 2 or 3 like this. Rental Rules call for a minimum rental of 2 weeks, with up to 24 rentals per year. The 2 week restriction is a good compromise between the really limited 1-month minimums and the really aggressive shorter terms. Owners can get up to $40,000+ gross after building up cliental and avoiding winter season themselves. Or owners can utilize some peak months themselves and still get some rental income. Appreciation is also good as these units avoid the "hotel" label and have many full-time residents living in them.

(Siesta Key Examples: Crystal Sands)

"Vacation Rental" Condominiums (Best for Investors)

Rental Rules call for a minimum rental of 1 week, with up to 52 rentals per year. These are the most profitable units to own. Owners who rent as much as possible may be able to gross $45,000 - $75,000+ annually. These units tend to have few (if any) full-time residents; they are geared for maximum rental income. (And are the main subject of this book).

(Siesta Key Examples: Island House Beach Resort, Fisherman's Cove)

"Vacation Rental Hotel" Condominiums (Can be a great Investment)

Rental Rules call for a minimum rental of 1-3 nights, as any times as possible per year. Typically these units have no full-time residents, and are totally geared for short-term rentals. While some are very nice, they may tend to be slightly less expensive or desirable than the 1 week minimum condos. But like all of Siesta Key, their values continue to grow.

(Siesta Key Examples: Sea Crest, Crescent Towers)

Your Planned Usage and the "neighborhood"

As you examine the 5 general categories above, it should be very apparent that "Minimum Rental Period" allowed in the condo docs clearly spells out each ones' potential annual gross rental incomes. (And serious investors should only consider the bottom 3). But these minimum rental periods also strongly set the environment you will be surrounded with when you visit your unit!

In the "Residential" types, you will likely learn who your fellow owners are; perhaps become friends, enjoy their company over the years, and in general during your stay, live in a relatively secluded private "club". There will be few (if any) renters, (and their young kids). In general your visit will be the most relaxing. When you visit in the off-months (summer, fall), the complex will be close to empty. But the tradeoff for this is that you will receive the least rental income. But if you are not worried about mortgage payments, you still can look forward to appreciation over the years of your Ocean front property.

In the "Investor" type units, your visits will be more like hotel stays (regardless of the length of your stay). Most weekends will be "change over", with tenants leaving and new ones arriving. Lobbies may be crowded, elevators crowded, and parking confused. There will be families who saved for a year to pay for this week on the beach, looking to squeeze the most bang for their buck! (And you'll love it, because you'll see "$$$$" and realize all this fun enjoyed by so many folks from all over the world is helping make your mortgage payments!

The Compromises

To my knowledge there currently are only 2 Condominiums on Siesta Key that fall into that "compromise" area, (With minimum rental periods of 2-weeks) Crystal Sands and Excelsior. Depending upon your view, these are either the best choices or the worst, investors may see it differently.

They tend to have more permanent residents and fewer vacationing families, making for a good compromise between generating some income while avoiding the downsides of too many teens, kids, and visitors, clogging up everything

As a proud owner at Crystal Sands, (We Crystal Sands owners consider our condo one of the most desirable (And certainly most noticeable) venues on Siesta Beach for many reasons including our "Ocean Front Pool"), I have enjoyed stable annual rental income in the $39,000 to $45,000 area, and if and when I sell it, look forward to making back many times my original down payment. (Also it should be noted that some Crystal Sands owners enjoy much higher annual incomes as some have invested in premium interiors and charge premium rates).

Condominium Carrying Costs vs. Rental Incomes

Interestingly there is little if any relationship between the purchase price of a given Condo unit and its gross rental income. In other words, regardless of whether you buy a unit that will gross $15,000 per year, or $70,000 per year, likely the Quarterly Condo Maintenance Fee, the Real Estate Taxes, and the Insurance costs will all be in about the same ballpark.

Important Considerations: An On-Site Rental Office

If your plan is to purchase a Vacation Rental unit mostly as an investment and you live out-of-state (As I did), you may want to focus on Condominiums that have an "On-Site" Rental Office directly on their property.

In the typical arrangement, you will sign a one-year agreement with the Rental Office to let them serve as your "Rental Agent" exclusively. They will advertise (to some limited extent), the properties, seek and book renters for your unit, collect all fees, pay all local taxes, schedule all cleanings, and mail you a monthly statement and check. For this service, they will charge you a standard "rental commission" and subtract it, along with any other expenses (like cleaning, repairs, or supplies) you have for the given rental period, and mail you the net. Note that some (but not all) Rental Offices will deposit your rental proceeds check at your bank directly.